Divorce introduces significant complexity into virtually every aspect of financial life, and tax filing is no exception. One of the most contested issues divorcing or separated parents face is determining which parent has the right to claim shared children as dependents on their federal tax return. This determination carries substantial financial implications, as dependency claims directly affect eligibility for valuable tax credits and deductions.

Understanding the Internal Revenue Service (IRS) rules governing dependent claims can help parents avoid costly filing errors, prevent processing delays, and ensure compliance with federal tax law. This comprehensive guide outlines the regulations that determine which parent claims the dependents, the process for transferring dependency rights, and the specific tax benefits associated with each scenario.

The Custodial Parent Rule: Understanding the Default Position

The IRS establishes a clear default rule for determining which parent may claim a child as a dependent following a divorce or separation. The custodial parent: defined as the parent with whom the child lived for more than half of the tax year: holds the primary right to claim the child as a dependent.

This determination is based purely on physical custody, meaning the number of nights the child spent residing with each parent during the calendar year. The IRS does not consider factors such as:

- Which parent provides greater financial support

- What the divorce decree or custody agreement states about tax claims

- Which parent pays child support

- The parents' respective incomes

Only one parent may claim the same child as a dependent in any given tax year. Attempting to claim a child who has already been claimed by the other parent will result in IRS scrutiny, delayed refund processing, and potential penalties.

Determining Custodial Parent Status: The Night Count Test

The IRS applies a straightforward "night count" test to establish which parent qualifies as the custodial parent. Tax professionals and parents should track the following:

Primary Residence Calculation:

- Count the total number of nights the child spent at each parent's residence during the tax year

- The parent with the greater number of nights is designated the custodial parent

- Nights the child spends at school, camp, or with relatives generally count toward the parent with whom the child would have stayed

Equal Custody Situations:

When the child spends an exactly equal number of nights with each parent during the tax year, the IRS applies a tiebreaker rule. In these cases, the parent with the higher adjusted gross income (AGI) is considered the custodial parent for purposes of claiming the dependency exemption.

Parents should maintain accurate records of custody schedules throughout the year, as documentation may be required if the IRS questions the dependency claim.

Form 8332: Releasing the Dependency Claim to the Non-Custodial Parent

While the custodial parent holds the default right to claim the child, the IRS permits this right to be transferred to the non-custodial parent through a formal process. Form 8332, Release/Revocation of Release of Claim to Exemption for Child by Custodial Parent, serves as the official mechanism for this transfer.

How Form 8332 Works

The custodial parent must complete and sign Form 8332 to release their claim to the dependency exemption. The form allows for flexibility in the transfer arrangement:

- Single-year release: The custodial parent releases the claim for one specific tax year only

- Multi-year release: The custodial parent releases the claim for a specified number of consecutive years

- Permanent release: The custodial parent releases the claim for all future years until revoked

The non-custodial parent must attach the signed Form 8332 (or a similar written declaration containing all required information) to their tax return when claiming the child as a dependent.

Important Considerations for Form 8332

Parents should understand several critical points about the dependency release process:

Divorce decrees do not automatically transfer dependency rights. Even if a divorce agreement stipulates that the non-custodial parent may claim the child, Form 8332 must still be executed for IRS purposes.

The release can be revoked. A custodial parent who previously signed a multi-year or permanent release may revoke that release for future years by completing Part III of Form 8332.

Both parents should retain copies. The custodial parent should keep a copy of the signed form, and the non-custodial parent should keep the original with their tax records.

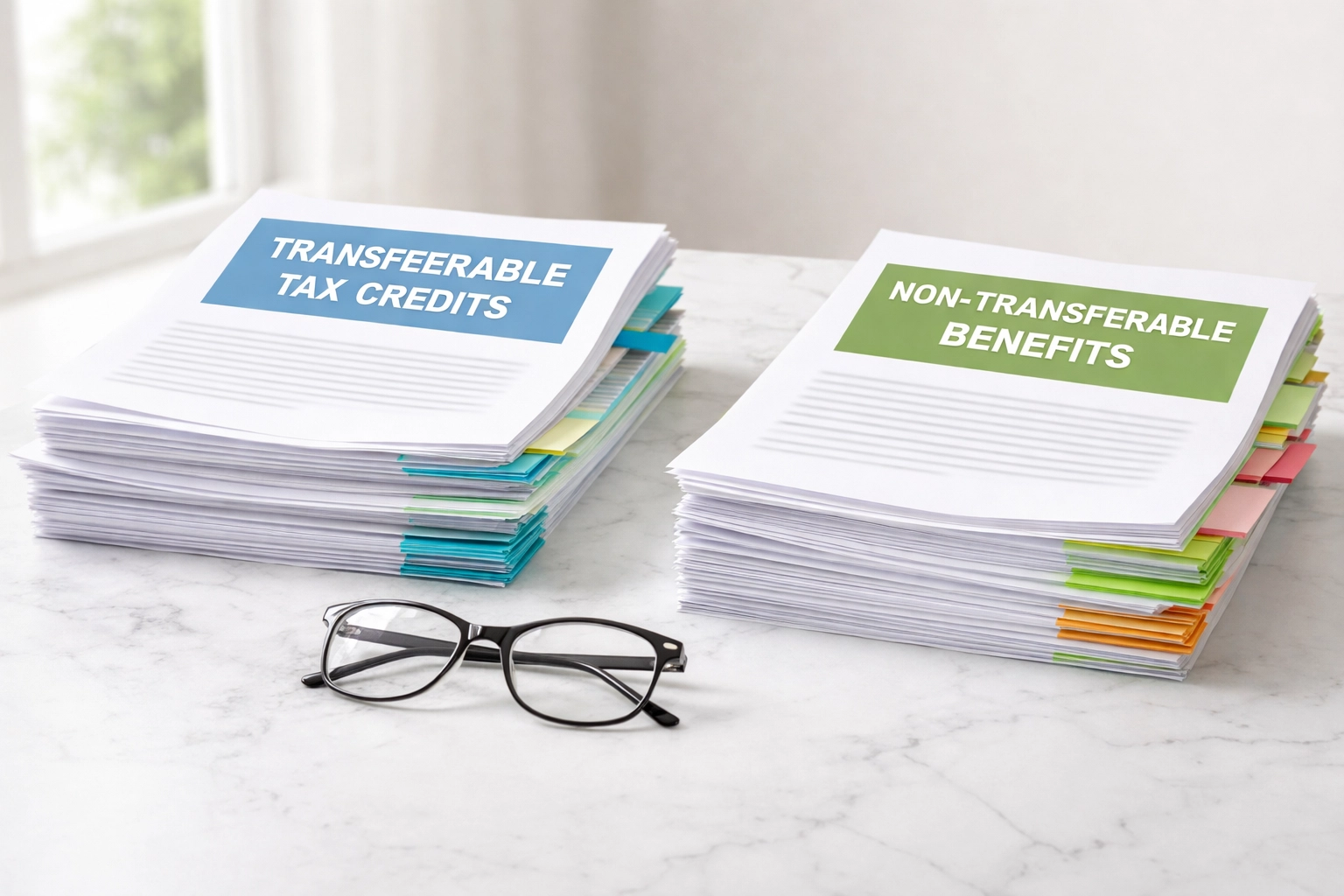

Tax Benefits: What Transfers and What Remains

One of the most misunderstood aspects of dependency claims in divorce situations involves which tax benefits transfer with the dependency exemption and which remain exclusively with the custodial parent. Form 8332 does not transfer all child-related tax benefits.

Tax Benefits That Transfer to the Non-Custodial Parent

When the custodial parent releases the dependency claim via Form 8332, the following credits and benefits may be claimed by the non-custodial parent:

- Child Tax Credit – Up to $2,000 per qualifying child

- Additional Child Tax Credit – The refundable portion of the Child Tax Credit

- Credit for Other Dependents – $500 for qualifying dependents who do not qualify for the Child Tax Credit

Tax Benefits That Remain With the Custodial Parent

Regardless of which parent claims the dependency exemption, certain tax benefits remain exclusively available to the custodial parent:

- Earned Income Tax Credit (EITC) – A significant refundable credit for low-to-moderate income workers

- Child and Dependent Care Credit – Credit for childcare expenses incurred while the parent works or seeks employment

- Head of Household Filing Status – A more favorable filing status with higher standard deductions and lower tax rates

This distinction is critical for tax planning purposes. Parents should carefully evaluate which arrangement provides the greatest combined tax benefit for the family unit, particularly when one parent qualifies for the EITC and the other does not.

When Both Parents Claim the Same Child

Despite clear IRS rules, situations arise where both parents mistakenly: or intentionally: claim the same child as a dependent on their respective tax returns. When this occurs, the IRS employs tiebreaker rules to determine which parent's claim takes priority.

IRS Tiebreaker Rules

The IRS applies the following hierarchy when resolving duplicate claims:

- Custodial parent prevails – The parent with whom the child lived for the greater number of nights during the tax year

- Higher AGI prevails – If the child spent equal time with both parents, the parent with the higher adjusted gross income

- Earlier filed return may be processed first – However, this does not determine the legitimate claim; the IRS may later adjust or reject the improper claim

Consequences of Duplicate Claims

When both parents claim the same dependent, both tax returns will be flagged for review. This typically results in:

- Significant delays in refund processing

- IRS correspondence requiring documentation of custody arrangements

- Potential assessment of additional taxes, interest, and penalties against the parent who filed improperly

- Possible requirement to amend the tax return

Parents should communicate clearly about dependency claims before filing to avoid these complications.

Practical Recommendations for Divorced or Separated Parents

Proper planning and documentation can prevent disputes and ensure compliance with IRS regulations. The following practices are recommended:

Maintain Detailed Custody Records

- Keep a calendar documenting which parent had physical custody each night

- Save text messages, emails, or other communications that verify custody arrangements

- Retain copies of formal custody agreements and any modifications

Coordinate Tax Filing Strategies

- Discuss dependency claims with the other parent before filing

- Consider alternating years if appropriate for the family's financial situation

- Evaluate the combined tax benefit of different claiming arrangements

Formalize Agreements Properly

- Execute Form 8332 when releasing dependency claims

- Do not rely solely on divorce decree language for IRS purposes

- Keep signed forms with tax records for at least seven years

Seek Professional Guidance

- Consult with a qualified tax professional to understand the implications of different claiming arrangements

- Review tax situations annually, as income changes may affect optimal filing strategies

Conclusion

Determining which parent claims dependents after a divorce requires careful attention to IRS rules and proper documentation. The custodial parent holds the default right to claim the child, but this right can be transferred through Form 8332. Understanding which tax benefits transfer and which remain with the custodial parent enables families to make informed decisions that maximize their combined tax position.

Parents facing questions about dependency claims following divorce or separation should consult with a qualified tax professional. TIG Tax Services provides expert guidance on complex tax situations, including divorce-related filing concerns. For assistance with tax preparation and planning, visit TIG Tax Services to schedule a consultation.