Gig workers and small business owners have faced significant confusion over the past few years regarding Form 1099-K reporting thresholds. Between shifting IRS guidelines, delayed implementations, and recent legislative changes, many taxpayers remain uncertain about when they should expect to receive this form from payment platforms.

The current reporting threshold stands at $20,000 in payments AND at least 200 transactions for the 2025 tax year and beyond. This means the income gig workers received throughout 2025 will be reported to the IRS under this standard when platforms issue 1099-K forms in early 2026.

The History Behind the Confusion

The uncertainty surrounding Form 1099-K thresholds stems from years of planned changes and subsequent reversals. Understanding this timeline helps explain why so many gig workers remain confused about their reporting obligations.

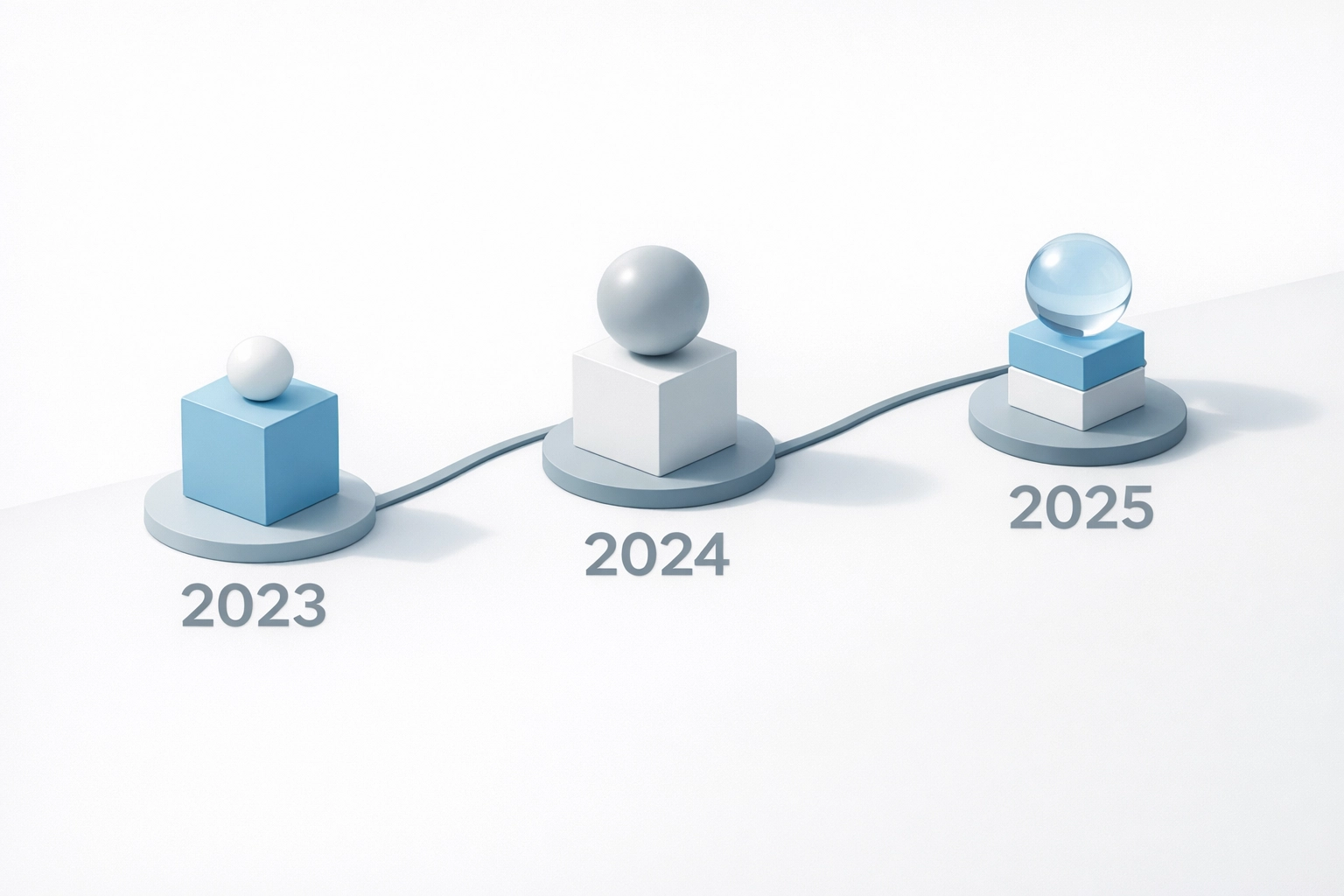

2023 Tax Year: The threshold remained at $20,000 in payments with a minimum of 200 transactions. This long-standing rule had been in place for years, creating stability for both payment platforms and their users.

2024 Tax Year: The IRS lowered the threshold to $5,000 with no transaction minimum requirement. This change represented a significant shift, as it eliminated the transaction count requirement entirely.

Originally Planned for 2025-2026: The IRS had announced intentions to lower the threshold progressively: dropping to $2,500 for the 2025 tax year, then down to $600 for 2026. This phased approach aimed to gradually adjust taxpayers and payment platforms to the new reporting requirements.

Current Rule (2025 and Forward): The passage of the One Big Beautiful Bill in July 2025 reversed these planned decreases. Congress permanently set the threshold back to $20,000 with the 200-transaction minimum reinstated. This legislative action ended years of uncertainty and provided long-term clarity for gig workers and payment platforms.

What Form 1099-K Actually Reports

Form 1099-K reports payment card transactions and third-party network transactions. Payment platforms like Venmo, PayPal, Square, Cash App, Stripe, and similar services must issue this form when users meet the reporting thresholds.

The form tracks gross payments received through these platforms. It does not account for:

- Business expenses or costs of goods sold

- Refunds or chargebacks

- Personal transfers between friends and family

- Reimbursements

Taxpayers should understand that receiving a 1099-K does not automatically mean they owe taxes on the full amount shown. The form simply reports the total payments processed through the platform.

Current Thresholds Explained

Under the current rules, gig workers and small business owners will receive Form 1099-K from payment platforms only when they meet both of these conditions:

- Total payments exceed $20,000 during the calendar year

- Account activity includes more than 200 separate transactions

Missing either threshold means no 1099-K will be issued. For example, a freelancer who received $25,000 through only 150 transactions would not receive the form because the transaction count falls below the 200-transaction minimum. Similarly, someone with 250 transactions totaling $18,000 would not receive the form because the payment amount falls short of the $20,000 threshold.

What This Means for Gig Economy Workers

The higher threshold provides substantial relief for casual sellers, part-time gig workers, and those with smaller transaction volumes. Individuals selling occasional items online, providing sporadic freelance services, or supplementing their income through gig platforms may fall below these thresholds.

However, taxpayers must recognize a critical point: not receiving a 1099-K does not eliminate tax obligations. All income remains taxable regardless of whether a taxpayer receives a reporting form. The IRS requires individuals to report all income on their tax returns, even when they do not receive documentation from payers.

Income Reporting Requirements Without a 1099-K

Gig workers who earn income below the 1099-K thresholds still must report that income on their tax returns. The form serves as a reporting mechanism for the IRS to verify income, but its absence does not change fundamental tax obligations.

Self-employed individuals and independent contractors should report income on Schedule C (Form 1040). This schedule allows taxpayers to document business income and claim legitimate business expenses, reducing taxable income.

Rideshare drivers, delivery workers, freelancers, online sellers, and other gig workers should maintain detailed records of all income received throughout the year. Relying solely on 1099-K forms can lead to underreporting, which may trigger IRS scrutiny or penalties.

Proper Income Tracking Practices

Given that 1099-K forms may not capture all income sources, gig workers should implement robust record-keeping systems. Effective practices include:

Maintain Separate Bank Accounts: Using dedicated business accounts helps separate personal and business transactions, simplifying record-keeping and providing clear documentation during tax preparation.

Track All Payment Methods: Income may arrive through various channels: direct deposits, checks, cash payments, and multiple payment platforms. Comprehensive tracking ensures no income goes unreported.

Save Platform Statements: Payment platforms typically provide transaction histories and annual summaries. These documents serve as valuable backup documentation even when they do not issue formal 1099-K forms.

Record Business Expenses: Tracking deductible expenses remains equally important. Mileage, supplies, equipment, home office costs, and other legitimate business expenses can significantly reduce taxable income.

Use Accounting Software: Digital tools and apps designed for self-employed individuals automate much of the tracking process, categorize transactions, and generate reports that simplify tax preparation.

When 1099-K Amounts Appear Incorrect

Payment platforms occasionally make errors when generating 1099-K forms. Common issues include reporting personal transfers as business income or including refunded transactions in the total amount.

Taxpayers who identify discrepancies should contact the payment platform immediately to request a corrected form. The platform may issue a corrected 1099-K that accurately reflects taxable business income.

When corrections cannot be obtained before the tax filing deadline, taxpayers should report the correct income amount on their tax return and maintain documentation explaining the discrepancy. A detailed record of the error and attempts to correct it provides important protection during potential IRS inquiries.

Understanding Personal vs. Business Transactions

One significant source of confusion involves distinguishing personal transfers from business payments. Friends splitting dinner costs, family members reimbursing expenses, or roommates sharing rent do not constitute taxable business income.

Most payment platforms now allow users to categorize transactions as personal or business. Properly categorizing transactions helps platforms accurately calculate reportable amounts and reduces the likelihood of receiving inflated 1099-K forms.

Taxpayers should review their platform settings and transaction histories to ensure proper classification. Correcting misclassified transactions before year-end prevents complications during tax season.

Looking Ahead: Long-Term Stability

The legislative action establishing the $20,000 and 200-transaction threshold provides welcome stability after years of uncertainty. Gig workers can now plan their record-keeping and tax strategies with confidence that the rules will remain consistent in coming years.

This consistency benefits not only individual taxpayers but also payment platforms, tax professionals, and the IRS itself. Clear, stable rules reduce administrative burdens and help all parties manage their obligations more effectively.

Professional Tax Assistance

The complexities of gig economy taxation extend beyond 1099-K reporting thresholds. Self-employed individuals face quarterly estimated tax payments, self-employment tax calculations, business expense documentation, and various other requirements that differ significantly from traditional W-2 employment.

Working with experienced tax professionals helps gig workers navigate these complexities, identify all available deductions, ensure accurate reporting, and avoid costly mistakes. Tax professionals stay current with changing regulations and provide guidance tailored to individual circumstances.

TIG Tax Services specializes in helping gig workers, freelancers, and self-employed individuals manage their tax obligations effectively. The firm's expertise ensures clients maximize deductions, maintain proper documentation, and file accurate returns that minimize tax liability while maintaining full compliance with IRS requirements.

Key Takeaways

The 1099-K reporting threshold currently stands at $20,000 in payments and at least 200 transactions. This threshold applies to income received during 2025 and future years. Gig workers who fall below either threshold will not receive Form 1099-K from payment platforms, but they remain obligated to report all income on their tax returns.

Proper record-keeping practices, clear separation of personal and business transactions, and professional tax guidance help gig workers navigate their obligations confidently. Understanding these rules and maintaining organized records throughout the year simplifies tax preparation and ensures compliance with IRS requirements.